Isn't rental income treated as income tax? It is in the U.S. Since tax is on the profit only, the tax would be on that 40%, so 32% of 40% so ~10%. You are still walking away with 68% of 40%, so 30% of your rental income is profit.

It is not. It is pure capital gains tax. Actually it is worse than that, because it can be difficult to prove what your true gains are. Loan costs for example are not easily tax-deductible, you must establish a firm for that.

I gave up landlording altogether, because for many years it was not worth the hassle. Most areas in Helsinki it is more profitable to keep the apartment empty and wait for the rich Russian, who buys it at +50%. In this building third of the apartments are empty or short-time rentals of some sort.

right but I'm guessing a huge percentage is baby boomers or Gen X'ers who bought a house 10 or more years ago. I'm curious to see a graph of home ownership rate history for people between 25 and 39 years old, I'm guessing it is lower now than 30 years ago.

The only numbers I could find about this disagree with you:

> Just 47.9% of U.S. millennials owned homes in 2020, according to Apartment List analysis of census data. At age 30, millennial home ownership hit 42%, compared with 48% for Gen Xers and 51% for baby boomers.

In defense of Bitcoin, it would have taken a decade to process the $40 billion of withdrawals from SVB on the blockchain, so a bank run couldn't have happened.

hmm, i saw somewhere that svb had some 37000 depositors

there's no relevant limit to the amount of money in a bitcoin transaction, so this could have been one transaction with 37000 outputs, or 37000 transactions one output, or 370 transactions with 100 outputs, or whatever

the latest block in the bitcoin blockchain is block 780'537 https://www.blockchain.com/explorer/blocks/btc/780537 containing 1788 transactions, totaling 4489.31 bitcoin, which is currently about 98 million dollars; the block weighs 1847 kilobytes

most of these transactions had 2 outputs, though many had more (7, 8, 9, 20) and a few had only 1. if we estimate this block as containing 3700 outputs we wouldn't be far wrong. in that case it would take 10 blocks (a little under two hours) to process all 37000 withdrawals

processing 200 billion dollars of transactions at the rate that money was being transferred in this block would take 2000 blocks, almost two weeks, because the average transaction size in this block was much smaller than svb's average account size; this is still less than a decade

consider transaction a400f39693ab997c162156a09599557b26c7a6d1efa711c49f4ccf5b12505b66 https://btcscan.org/tx/a400f39693ab997c162156a09599557b26c7a... with 21 outputs. this transaction is 837 bytes, so it's a little smaller than average for this block despite its large number of outputs; an 1837-kilobyte block consisting only of such transactions would contain 2206 transactions, paying out to 46326 different addresses

so in fact the bitcoin blockchain could have processed all of svb's withdrawals in a single block

the price of bitcoin would have to go up quite a bit for that to happen; bitcoin's market cap is currently only 389 billion dollars, so this one piddly bank would have been more than half of it, and transferring such a large amount of bitcoin around at once would likely freak people out enough to blow the whole system up

but there's no technical reason in the bitcoin blockchain that dissolving such a bank would be impossible or even difficult

there have been any number of bank runs in bitcoin already, unfortunately

If the treasury allowed a bank run to wipe out depositors, every single business would be transferring funds out of their regional bank Monday morning.

exactly, the idea is for depositors not to care if a bank run happens or not, because the way that bank runs happen is that depositors worry that a bank run will happen

I don't understand this comment. 1) SVB was not managed by VC's. 2) SVB went under because they bought US Treasuries, not because they took risky bets on startups.

I see it the other way around. The VCs started a panic. Name one other bank that could survive $42 billion in withdrawals in a single day. Other than Bank of Zimbabwe, obviously. Even Wells and JP Morgan would collapse under that strain. The VCs caused their own pain.

Yeah, but what are the specific cash amounts we are talking about?

Such extreme exposure to interest rate risk would've blown up in some other ways - say, a large client processing a routine payroll, executing stock buyback, or investing in an entity that banks elsewhere.

SVB had risks, VCs did what they should do to respond to said risk. Would you blame regular working class people in a retail bank run scenario for wanting to save their money from potential risk?

No. SVB price crashed 50% in one day and got downrated by Moodys, which exposed a bunch of red flags that would have resulted in a bank run regardless of what VCs said.

The stock crashed because of the initial pseudo bank run due to high interest rates on capital (at least that's the reason given for withdrawals), and the bank's subsequent failure to make up the difference after selling a treasuries portfolio. After which a real bank run occurred. Then the bank started down a path of a more desperate measure, and that's when they were shut down. At least that's what I got from an article.

1. If they had more short dated treasuries, they could have used them to fund drawdowns, and would not have had to sell their long dated treasuries, that went underwater as interest rates rise.

2. If they had not been overly exposed to one sector, a sector that largely existed due to 'free money' of zero interest rates, then large scale draw downs would not have happened as interest rates rise.

YC asked for exactly what just happened. (Depositors be made whole.) They did not ask for anything beyond what regulators ultimately deemed reasonable.

I think this is very much in question. Silicon Valley Bank was absolutely part of a cohesive microeconomy. There's no other explanation for the absolutely uniformity with which all those startups were using it for what should have been 100% commodity banking services. Those startups all banked with SVB because their VCs told them to.

And the VCs told their startups to bank with SVB because... we don't know yet. But any time you have a signal this strong, there's a driver.

Add to that the fact that the moment all those startups seemed likely to lose banking services, however temporarily, those same VCs freaked the fuck out of their minds on twitter and started shrieking in all caps about the end of western capitalism. That's not mere concern for their poor startups (most of whom were going to fail anyway, after all -- they're startups!). These VCs were exposed to the SVB failure. They were leveraged somehow and about to get caught holding the bag.

There was some kind of insider dealing going on with SVB. It wasn't just a bank. We for sure know that much. Whether we have criminal fraud or not is an open question.

SVB made loans to cash-rich companies approximate to their funding rounds, when they were least likely to immediately use the cash. These loans typically required the company to hold the money as a deposit in SVB. These deposits were used to buy long duration bonds.

In other words, SVB used these companies to produce new money that they could earn interest on.

Yeah, that's the kind of thing I'm imagining. Though it doesn't explain the VC tweetpanic unless they were getting kickbacks. Is there a cite for that, or a story posted somewhere?

One element is that the banking industry as a whole behaves pretty chaotically with 'unusual' customers.

Big wire in from a fundraising round? Account frozen. Big wire out for an acquisition? Account frozen. Bank learns your customers include cryptocurrency companies? Account frozen. Bank account balance huge relative to your business' cashflow? Account frozen. Random bank staff doesn't understand what you're doing? Account frozen.

In that kind of climate its almost inevitable that VC's would recommend a single bank known to not behave erratically for the activities that are usual for their investments.

"I just hope nobody forgets how prominent VCs behaved during the brief period of uncertainty."

The point is that these VC's didn't act to support their investments, they flailed around begging for bailout (that they probably didn't need but they didn't understand banking well enough to know that or bother to consult any experts before making public statements).

They behaved badly and should be embarrassed and everyone should remember it.

Why do you find it believable that they asked for government intervention to protect "the innocent" as opposed to simply acting to protect their own private financial interests, which seems to be the simplest explanation?

I'm not even convinced that the depositors made whole here were innocent--they accepted a known risk by exceeding the risk-free FDIC limit. The sad part is that in our society, we have no qualms about literally turning working people out into the street when they make financial missteps, but the already-wealthy receive prompt intervention from the highest levels to protect them and other wealthy people from the consequences of their investment decisions.

What argument is really left for this kind of intervention, besides appeals to the trickle-down system where the rich must be vigilantly protected since the rest of our society is set up to be disrupted when they fail. The whole system is morally and politically bankrupt.

> Why do you find it believable that they asked for government intervention to protect "the innocent" as opposed to simply acting to protect their own private financial interests

They are the innocent party here though (well, except for maybe Peter Thiel). The depositors didn't cause this problem.

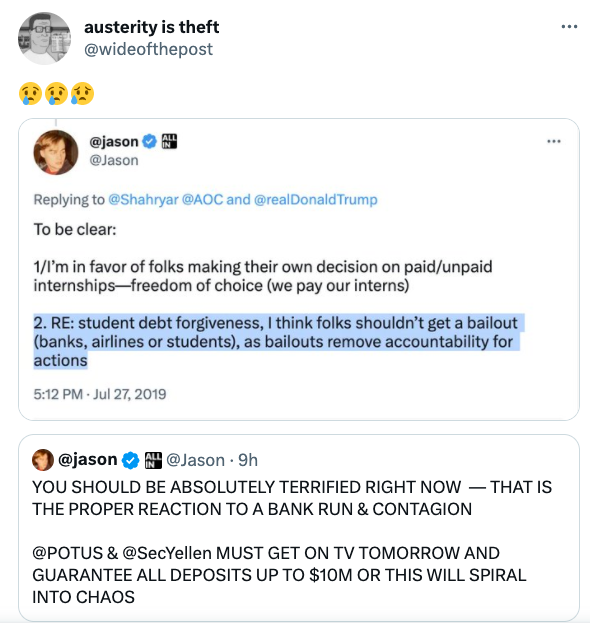

Being against student loan forgiveness or any sort of help to anyone, ever, but then running to mommy Yellen the second you get in trouble is just too hypocritical to believe.

If that's where you (philosophical you, not you personally) landed on those two issues, you can get fucked.

They begged for special dispensation that they didn't ever need. They proved themselves to be both selfish and ignorant and deserve any derision they receive.

This was an extremely obvious example of when the private sector could've collaborated to solve a problem. SVB was doing a capital raise just last week. Instead the VC community colluded to accelerate the problem and is now asking for a government bailout

What innocent? They could have sold the uninsured deposits at a discount, made payroll, and let the equity eat the loss. Instead they went on an embarrassing bailout begging extravaganza and unfortunately succeeded. Nobody, ever, should take any of these people seriously again.

They actually brewed up the contagion. Without the alarmism everyone would just assume that they get a 10-20% haircut and have most of their money back within a week

SVB regularly provides credit to risky startups, which is why they existed in the first place (because other banks wouldn't lend at those rates). So, yes, they sorta did place risky bets on startups.

Source for this? All evidence show that their failure at least started with them owning a lot of "safe" bonds, whose value declined with increasing fed rates.

Yes, long-term treasuries which for years had been at very low interest rates. You're certainly right that they shouldn't have done that, but it doesn't invalidate GP's point.

The fact that SVB just went under disproved your point. Without a moat a company is relegated to ways of making money that at some point in time become unsustainable (i.e. when interest rates change) and then go under. As opposed to companies with strong moats that defend their free cash flow (i.e. Apple).

It doesn't disprove it at all, because I'm certainly not arguing that not having a moat is a strength. It almost sounds like you are arguing that having a moat makes a company indestructible.

I don't understand, is it because they do not want to change its monetization to ads and IAP's? How is having this game in the App Store making them lose money?

Might want to specify https://www.workatastartup.com/ - if OP hasn't heard of it, your comment might be interpreted as just "working at a startup" in the general sense.

{kind=link}